My Unscientific Theory on Why the Recent Rise in Income Is Only the Bubble Trying to Work Its Way Through the System

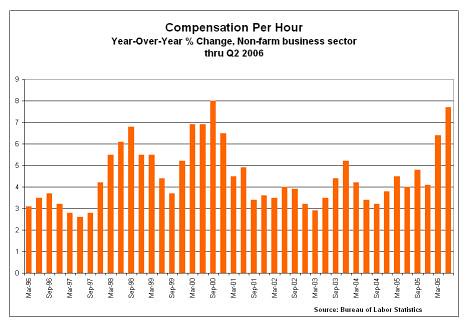

Here's a great chart showing a nice gain in compensation per hour, year-over-year percent change. Second quarter 2006 comes in at a nice 7.7%, which is good news for all those people who were complaining that their real incomes were not progressing. (Real increase is about 3.2% annually. That's not bad, much better than recent years.)

Click on graph for larger image.

[Thanks to Prudent Bear for the graph.]

And I do think this is good news, because according to My Own Conjectured Theory Of Monetary Credit Fiddling (MOCTOMCF), wages are the next to last indicator to rise in an over-expanding monetary climate, and it's about time the marshmallow fluff got down to the little guy. After all, he's been spending a lot more for houses and experiencing CPI increases over the years; why shouldn't he get the corresponding wage lift? He's been the low man on the totem pole for too long, paying more, earning less, while the upper guys get all the profit -- as is usual with inflationary waves.

And this time the expansion could have bypassed him altogether, as the global credit maelstrom raged through booming sectors around the world: Mortgages in China, mergers in Europe, currency manipulation in developing economies, leveraged derivative speculation worldwide, etc., blowing right over his head. That would have been a pity, because it is he who is the real engine of our economy, i.e. the working man and woman.

The last indicator to rise, according to MOCTOMCF, is general prices, or CPI -- although it's already at a pretty fat 4.5% (compound annual 3-months rate ending July 2006.) For reasons having to do with "[t]he vast ('elastic') supply of contemporary output (including imports, digital media, technology, telecommunications services, medical, education, financial services and 'services' generally) [that] works to restrain rapid general price index gains" (as Doug Noland at Prudent Bear notes), the CPI seems to have risen relatively quietly. And anyway the Fed is not looking at CPI but at core inflation, which came in at 3.2% recently. (See my upcoming post for a comment about that.)

According to MOCTOMCF, this second stage of credit inflation started in the 1990s. Up until then, when in around 1980 the Fed realized the 20th century inflation game was catching up with them, they began reigning in credit, and things began to slow back to normal -- or almost. But it was too painful. In the early 1990s, just as the floodwaters had begun to dissipate in earnest, the Fed got impatient and started to pump credit back into the system, probably most significantly around 1993-4 and thereafter in spurts. Credit dollars blew into the tech stock market first; then when the bubble burst (as all bubbles do eventually), and instead of the Fed trying to sweep up the mess and starting over, they began re-inflating credit in early 2001. They were worried about not being liked, I guess. Or maybe a bite of the hair off the dog that bit you. Who knows.

So this time, the newly created credit flowed into the real estate market, the stock market having proven itself to be skittish. Home prices skyrocketed. In 2004, the Fed decided to slow things down again. But this time, the waters are not responding. Their contracting action was "measured" (how many times did we hear that word over the last four years?) So instead of turning off the faucet, credit was allowed to continue to bubble into the banking system even as the Fed was signaling a slow-down. But they weren't eliminating or reversing credit; they were just slowing down the bubbling -- which might explain the plethora of corporate profits and cash floating around, by the way, because corporations were just heeding the Fed's warnings about credit contraction and not investing in expansion, but the contractions just weren't materializing as fast as expected. Right now, they're in holding mode, waiting to see what the Fed will do next.

At this point, the Fed is thinking that credit must have stabilized; but the real estate and other credit markets (leveraged financial stuff, M&A, etc.) are still chugging defiantly uphill, like a huge 100-car freight train with the brakes on but the motor still running. By this time, inertia has taken over, and it would take a sudden jump in brake pressure (upping the Fed rate a few more times, for example) to have any real downward effect.

If the Fed stays where they are, the fluff will spread around the whole economy and things will get back to a statis of sorts; but of course they'll feel obliged to DO SOMETHING. Question is, what'll it be? The best thing would be for them to curl up and go to sleep like the Sleeping Beauty who never wakes up; but I'm afraid that's just not their style.

Doug Noland's 9/8/06 analysis is great, as usual. He notes the following data, relevant to MOCTOMCF:

"Year-to-date, Bank Credit has expanded $546 billion, or 10.8% annualized."

"Commercial & Industrial (C&I) Loans have expanded at a 16.5% rate y-t-d and 14.7% over the past year."

"Money Fund Assets have increased $168 billion y-t-d, or 11.8% annualized, with a one-year gain of $265 billion (13.5%)."

"Total Commercial Paper jumped $16 billion last week to a record $1.860 Trillion. Total CP is up $219 billion y-t-d, or 19.3% annualized, while having expanded $272 billion over the past 52 weeks (17.1%)."

“ 'Multinational companies will invest $1.2 trillion worldwide this year, the London-based Times said, citing a report by the Economist Intelligence Unit. The investment would be a 22 percent increase from last year…' " (from Bloomberg 9/6/06, Bill Murray)

He also offers this analysis:

"Continued robust mortgage borrowings and huge ongoing corporate and government debt growth combine for Record Total System Credit growth, this despite the significant decline in home sales transactions. The unrelenting massive Credit expansion – pursuant to several years of an intensifying Inflationary Bias permeating the wages and Incomes arena - readily explains today’s heightened Income Inflation. Record Total Credit Growth, then, continues to buttress home prices, in the process bolstering the Aged Credit Bubble and its brethren, the stock market Bubble."

Yup. All of this corroborates my MOCTOMCF. Now if only it were scientific. Rats.

Because I suppose there is a slight chance that this whole bubble-like expansion is nothing but productivity gain, as the Fed would have us believe. But somehow, I doubt it. And history is on my side.

Click on graph for larger image.

[Thanks to Prudent Bear for the graph.]

And I do think this is good news, because according to My Own Conjectured Theory Of Monetary Credit Fiddling (MOCTOMCF), wages are the next to last indicator to rise in an over-expanding monetary climate, and it's about time the marshmallow fluff got down to the little guy. After all, he's been spending a lot more for houses and experiencing CPI increases over the years; why shouldn't he get the corresponding wage lift? He's been the low man on the totem pole for too long, paying more, earning less, while the upper guys get all the profit -- as is usual with inflationary waves.

And this time the expansion could have bypassed him altogether, as the global credit maelstrom raged through booming sectors around the world: Mortgages in China, mergers in Europe, currency manipulation in developing economies, leveraged derivative speculation worldwide, etc., blowing right over his head. That would have been a pity, because it is he who is the real engine of our economy, i.e. the working man and woman.

The last indicator to rise, according to MOCTOMCF, is general prices, or CPI -- although it's already at a pretty fat 4.5% (compound annual 3-months rate ending July 2006.) For reasons having to do with "[t]he vast ('elastic') supply of contemporary output (including imports, digital media, technology, telecommunications services, medical, education, financial services and 'services' generally) [that] works to restrain rapid general price index gains" (as Doug Noland at Prudent Bear notes), the CPI seems to have risen relatively quietly. And anyway the Fed is not looking at CPI but at core inflation, which came in at 3.2% recently. (See my upcoming post for a comment about that.)

According to MOCTOMCF, this second stage of credit inflation started in the 1990s. Up until then, when in around 1980 the Fed realized the 20th century inflation game was catching up with them, they began reigning in credit, and things began to slow back to normal -- or almost. But it was too painful. In the early 1990s, just as the floodwaters had begun to dissipate in earnest, the Fed got impatient and started to pump credit back into the system, probably most significantly around 1993-4 and thereafter in spurts. Credit dollars blew into the tech stock market first; then when the bubble burst (as all bubbles do eventually), and instead of the Fed trying to sweep up the mess and starting over, they began re-inflating credit in early 2001. They were worried about not being liked, I guess. Or maybe a bite of the hair off the dog that bit you. Who knows.

So this time, the newly created credit flowed into the real estate market, the stock market having proven itself to be skittish. Home prices skyrocketed. In 2004, the Fed decided to slow things down again. But this time, the waters are not responding. Their contracting action was "measured" (how many times did we hear that word over the last four years?) So instead of turning off the faucet, credit was allowed to continue to bubble into the banking system even as the Fed was signaling a slow-down. But they weren't eliminating or reversing credit; they were just slowing down the bubbling -- which might explain the plethora of corporate profits and cash floating around, by the way, because corporations were just heeding the Fed's warnings about credit contraction and not investing in expansion, but the contractions just weren't materializing as fast as expected. Right now, they're in holding mode, waiting to see what the Fed will do next.

At this point, the Fed is thinking that credit must have stabilized; but the real estate and other credit markets (leveraged financial stuff, M&A, etc.) are still chugging defiantly uphill, like a huge 100-car freight train with the brakes on but the motor still running. By this time, inertia has taken over, and it would take a sudden jump in brake pressure (upping the Fed rate a few more times, for example) to have any real downward effect.

If the Fed stays where they are, the fluff will spread around the whole economy and things will get back to a statis of sorts; but of course they'll feel obliged to DO SOMETHING. Question is, what'll it be? The best thing would be for them to curl up and go to sleep like the Sleeping Beauty who never wakes up; but I'm afraid that's just not their style.

Doug Noland's 9/8/06 analysis is great, as usual. He notes the following data, relevant to MOCTOMCF:

"Year-to-date, Bank Credit has expanded $546 billion, or 10.8% annualized."

"Commercial & Industrial (C&I) Loans have expanded at a 16.5% rate y-t-d and 14.7% over the past year."

"Money Fund Assets have increased $168 billion y-t-d, or 11.8% annualized, with a one-year gain of $265 billion (13.5%)."

"Total Commercial Paper jumped $16 billion last week to a record $1.860 Trillion. Total CP is up $219 billion y-t-d, or 19.3% annualized, while having expanded $272 billion over the past 52 weeks (17.1%)."

“ 'Multinational companies will invest $1.2 trillion worldwide this year, the London-based Times said, citing a report by the Economist Intelligence Unit. The investment would be a 22 percent increase from last year…' " (from Bloomberg 9/6/06, Bill Murray)

He also offers this analysis:

"Continued robust mortgage borrowings and huge ongoing corporate and government debt growth combine for Record Total System Credit growth, this despite the significant decline in home sales transactions. The unrelenting massive Credit expansion – pursuant to several years of an intensifying Inflationary Bias permeating the wages and Incomes arena - readily explains today’s heightened Income Inflation. Record Total Credit Growth, then, continues to buttress home prices, in the process bolstering the Aged Credit Bubble and its brethren, the stock market Bubble."

Yup. All of this corroborates my MOCTOMCF. Now if only it were scientific. Rats.

Because I suppose there is a slight chance that this whole bubble-like expansion is nothing but productivity gain, as the Fed would have us believe. But somehow, I doubt it. And history is on my side.

posted by Katy Delay at 4:52 PM

![]()

![]()

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

0 Comments:

Post a Comment

<< Home