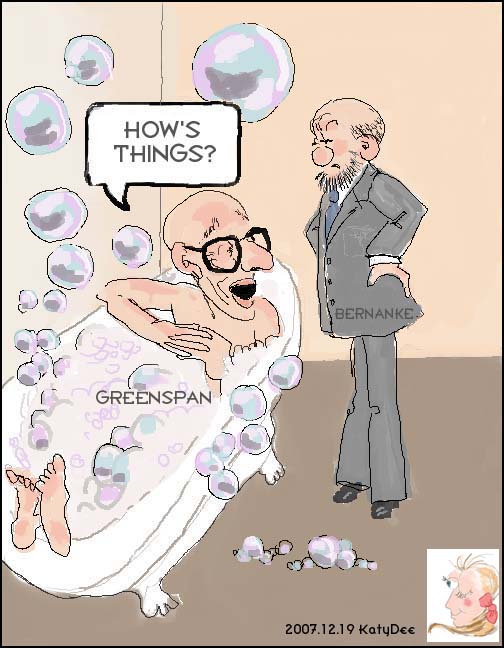

Balance of Payments: You Can't Fool All of the Market All of the Time

Foreigners are buying up US assets, most visibly those good-sized percentages of our flagship financial houses. I hear cries of horror around me, as though some rat were trying to sneak out the door with the Christmas turkey.

[Thanks to bahasa-malaysia-simple-fun.com for this image.]

No, it's very simply market-balancing forces at work.

You don't remember this, but there was a time when nations held gold as reserves to back their currency and as international money for trade adjustments. In those days, purchases made between countries were settled on paper for a while; but then, on a regular basis, the accountants reconciled their books and a ship left the harbor of one or the other nation with a hold full of gold, to settle up.

Nowadays, we see no such reckoning of the books, but instead a ridiculously ever-increasing, multiple-zero figure of balance-of-payment debt (the "current account deficit"), or balance-of-payment credit on the other side of the equation, that just keeps on accruing and that has now almost reached a trillion of net debt owed by the US to other nations.

Using a different statistic, foreigners now hold something like 2 trillion dollars worth of treasury and other agency debt. It's as if we owed that much to the bank, so to speak, before deducting what others owe to us.

Remember Reagan's illustration of what a trillion is? “If you had a stack of $1,000 bills in your hands only 4 inches high, you would be a millionaire. A trillion dollars would be a stack of $1,000 bills 67 miles high.” (Source.) This kind of puts it into perspective.

Today, therefore, because there is no gold-for-currency backing system, there is no automatic accounting mechanism that forces countries to settle their accounts on a regular basis. But that doesn't mean that such reckoning will not take place at some point.

Well, that's what happening now. Creditor nations--Abu Dhabi and other Arab nations, Singapore, Japan, China, et al.--are getting sick of piling up dollar bills now that these pieces of paper are losing value. They've decided that before they become worthless, they might as well be put to use to acquire something.

They can't get gold, and because they still like American assets (thank goodness), they have decided to buy what looks cheap. What's the best deal on the market right now? Well, without making a thorough study of the question, I'd say we should look for companies that are in trouble. We certainly have a few of those lying around. How about Merrill Lynch, Citigroup, or Morgan Stanley? We can even find some European goods for sale in dollars, like UBS for example, a good Swiss banking asset.

We should see more of these acquisitions in the next year or so. Why, I'll bet you that by a dozen months from now they'll be buying apartments and houses in our big cities. Oh, wait a minute, I'm seeing news of a few sales already. I would guess that the party's just getting started.

[Thanks to bahasa-malaysia-simple-fun.com for this image.]

No, it's very simply market-balancing forces at work.

You don't remember this, but there was a time when nations held gold as reserves to back their currency and as international money for trade adjustments. In those days, purchases made between countries were settled on paper for a while; but then, on a regular basis, the accountants reconciled their books and a ship left the harbor of one or the other nation with a hold full of gold, to settle up.

Nowadays, we see no such reckoning of the books, but instead a ridiculously ever-increasing, multiple-zero figure of balance-of-payment debt (the "current account deficit"), or balance-of-payment credit on the other side of the equation, that just keeps on accruing and that has now almost reached a trillion of net debt owed by the US to other nations.

Using a different statistic, foreigners now hold something like 2 trillion dollars worth of treasury and other agency debt. It's as if we owed that much to the bank, so to speak, before deducting what others owe to us.

Remember Reagan's illustration of what a trillion is? “If you had a stack of $1,000 bills in your hands only 4 inches high, you would be a millionaire. A trillion dollars would be a stack of $1,000 bills 67 miles high.” (Source.) This kind of puts it into perspective.

Today, therefore, because there is no gold-for-currency backing system, there is no automatic accounting mechanism that forces countries to settle their accounts on a regular basis. But that doesn't mean that such reckoning will not take place at some point.

Well, that's what happening now. Creditor nations--Abu Dhabi and other Arab nations, Singapore, Japan, China, et al.--are getting sick of piling up dollar bills now that these pieces of paper are losing value. They've decided that before they become worthless, they might as well be put to use to acquire something.

They can't get gold, and because they still like American assets (thank goodness), they have decided to buy what looks cheap. What's the best deal on the market right now? Well, without making a thorough study of the question, I'd say we should look for companies that are in trouble. We certainly have a few of those lying around. How about Merrill Lynch, Citigroup, or Morgan Stanley? We can even find some European goods for sale in dollars, like UBS for example, a good Swiss banking asset.

We should see more of these acquisitions in the next year or so. Why, I'll bet you that by a dozen months from now they'll be buying apartments and houses in our big cities. Oh, wait a minute, I'm seeing news of a few sales already. I would guess that the party's just getting started.

Labels: balance of payments, current account deficit, dollar devaluation, economic humor, economics

posted by Katy Delay at 6:41 PM

0 comments

![]()

![]()

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}