Is the Dollar a Dwarf or a Midget?

A couple of charts not seen very often in the news are the ones you can create with some Fed dollar statistics. Two of these are the "Nominal Major Currencies Dollar Index" and the "Price-Adjusted Major Currencies Dollar Index." The Fed uses a complicated set of formulas to come up with these numbers and has been doing so since the early 1970's.

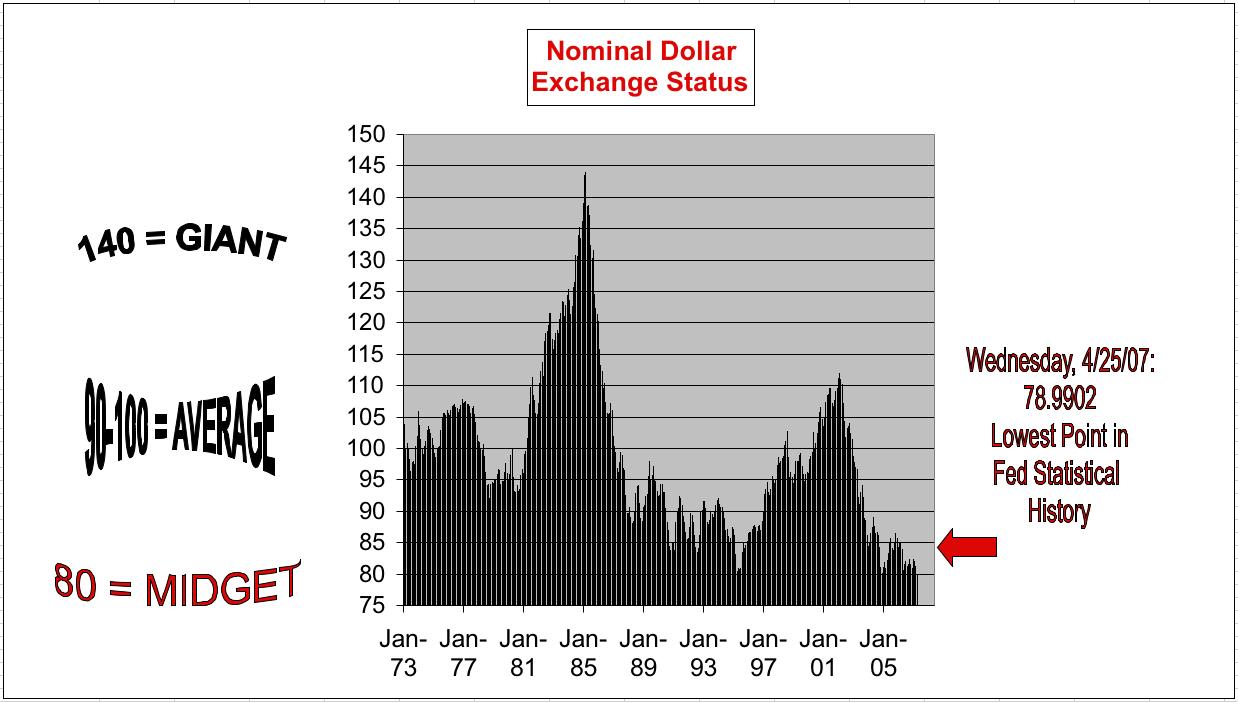

The "Major Currencies" indices are "a weighted average of the foreign exchange values of the U.S. dollar against a subset of currencies in the broad index that circulate widely outside the country of issue." [Source]

What is in that subset of foreign currencies? The euro (remember, that includes all the major European countries), the Canadian dollar, the Japanese yen, the British pound, the Swiss franc, the Australian dollar, and the Swedish krona.

I have made two charts showing the difference between the nominal chart and the inflation-adjusted one. The first shows us the actual exchange situation of the dollar today. (Click on the image to get a much larger version.)

As you can see, this month of April 2007, our dear dollar has hit rock bottom, at 78.9902 on the scale. [Source for the nominal chart.]

Here below, we have the inflation-adjusted version of this chart. This time, the different currencies have been weighted by the statisticians so that the degree of inflation in each country is reflected on the chart. In other words, here we have what the world sees as the US Tallest-Dwarf Status. The results are not quite so drastic.

But as you can see, and no matter how you look at it, the US dollar is getting smaller and smaller. We have been in a position to claim "Tallest Dwarf" status only twice in our more recent history (i.e. since 1973.) As of today, we are flirting with the loss of the title -- again. [Source for the price-adjusted chart.]

What I believe is unconscionable on the part of the central banks of this world, is that they are beginning to talk as though inflation is a necessary evil, something every nation must just "live with" and "make the best of." And now they're even talking as though our status as tallest dwarf were actually a handicap.

Meanwhile, the speculators are having a field day and the little guy is getting raked over the coals -- in other words, Big Financial Business as usual. (This reminds me of 1929....)

The "Major Currencies" indices are "a weighted average of the foreign exchange values of the U.S. dollar against a subset of currencies in the broad index that circulate widely outside the country of issue." [Source]

What is in that subset of foreign currencies? The euro (remember, that includes all the major European countries), the Canadian dollar, the Japanese yen, the British pound, the Swiss franc, the Australian dollar, and the Swedish krona.

I have made two charts showing the difference between the nominal chart and the inflation-adjusted one. The first shows us the actual exchange situation of the dollar today. (Click on the image to get a much larger version.)

As you can see, this month of April 2007, our dear dollar has hit rock bottom, at 78.9902 on the scale. [Source for the nominal chart.]

Here below, we have the inflation-adjusted version of this chart. This time, the different currencies have been weighted by the statisticians so that the degree of inflation in each country is reflected on the chart. In other words, here we have what the world sees as the US Tallest-Dwarf Status. The results are not quite so drastic.

But as you can see, and no matter how you look at it, the US dollar is getting smaller and smaller. We have been in a position to claim "Tallest Dwarf" status only twice in our more recent history (i.e. since 1973.) As of today, we are flirting with the loss of the title -- again. [Source for the price-adjusted chart.]

What I believe is unconscionable on the part of the central banks of this world, is that they are beginning to talk as though inflation is a necessary evil, something every nation must just "live with" and "make the best of." And now they're even talking as though our status as tallest dwarf were actually a handicap.

Meanwhile, the speculators are having a field day and the little guy is getting raked over the coals -- in other words, Big Financial Business as usual. (This reminds me of 1929....)

Labels: dollar, economics, economy, foreign exchange

posted by Katy Delay at 7:46 PM

0 comments

![]()

![]()

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}