Response to a Synical Swiss About the Dollar

Over dinner a few weeks ago, I was discussing the falling dollar with some friends, among whom was a Swiss economics journalist. He said something like, "But is the fall of the dollar really very important?"

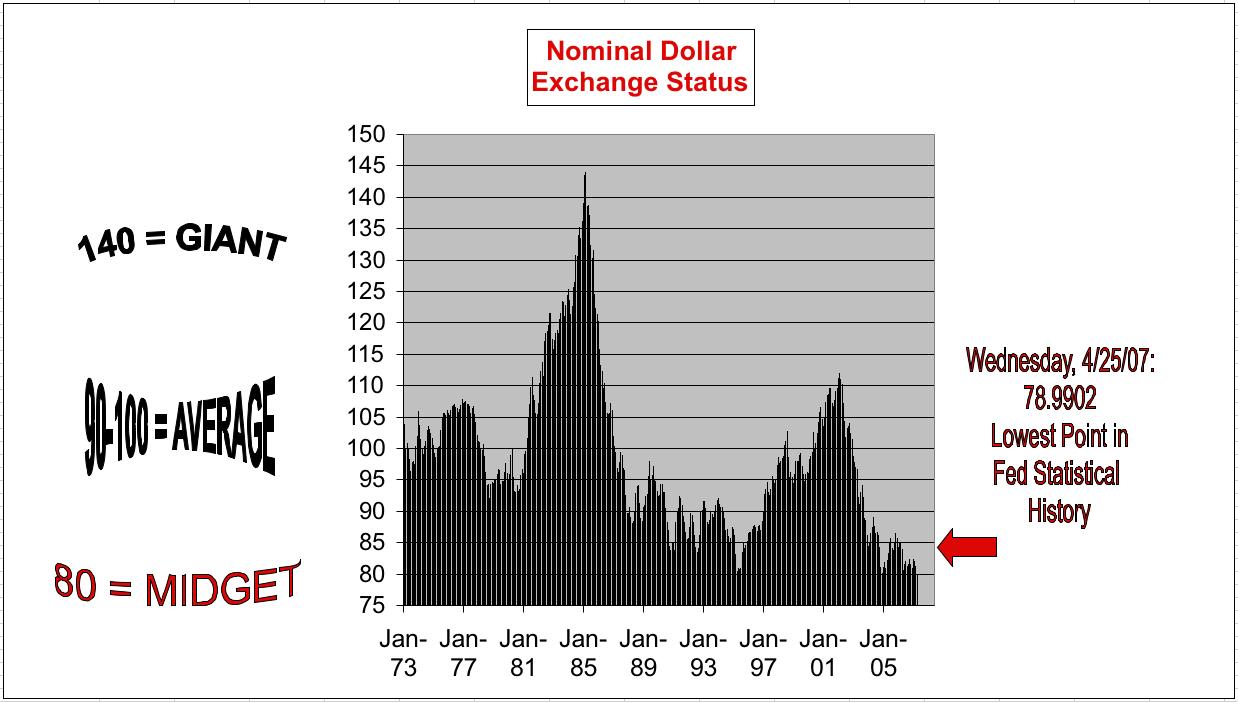

[Thanks to TradingCharts.com for the chart. Click on it for a larger version.]

I piped up that surely it was, if only because the value of the dollar was a kind of contract, a promise to pay and, given its reputation, a promise to remain a good store of value.

He replied, "But I don't think the dollar is a contract anymore. Everyone knows that currencies are floating, and that they are taking a calculated risk when they hold or invest in them."

I was shocked, even though I realized that technically he is correct. The dollar--in fact all currencies--are based on nothing other than our faith in them. They fluctuate today; everyone knows it. Yet I continue to hold that a strong dollar is in everyone's interest, not only those who travel abroad.

I tried to illustrate the kind of damages that were being done, giving the example of Saudi Arabia, where America has the privilege of buying oil in dollars that are getting weaker and weaker, and because of old agreements the Arabs have nothing to say about it. The conversation moved onto other subjects.

Today, I read this article in The Economist. The following sentence jumped out at me:

"The dollar's decline already amounts to the biggest default in history, having wiped far more off the value of foreigners' assets than any emerging market has ever done."

This speaks for itself, and somehow it carries more weight, coming off the black and white pages of a well-known economic magazine. I hope my Swiss journalist is reading it, too.

[Thanks to TradingCharts.com for the chart. Click on it for a larger version.]

I piped up that surely it was, if only because the value of the dollar was a kind of contract, a promise to pay and, given its reputation, a promise to remain a good store of value.

He replied, "But I don't think the dollar is a contract anymore. Everyone knows that currencies are floating, and that they are taking a calculated risk when they hold or invest in them."

I was shocked, even though I realized that technically he is correct. The dollar--in fact all currencies--are based on nothing other than our faith in them. They fluctuate today; everyone knows it. Yet I continue to hold that a strong dollar is in everyone's interest, not only those who travel abroad.

I tried to illustrate the kind of damages that were being done, giving the example of Saudi Arabia, where America has the privilege of buying oil in dollars that are getting weaker and weaker, and because of old agreements the Arabs have nothing to say about it. The conversation moved onto other subjects.

Today, I read this article in The Economist. The following sentence jumped out at me:

"The dollar's decline already amounts to the biggest default in history, having wiped far more off the value of foreigners' assets than any emerging market has ever done."

This speaks for itself, and somehow it carries more weight, coming off the black and white pages of a well-known economic magazine. I hope my Swiss journalist is reading it, too.

Labels: dollar, economic humor, economics, foreign exchange, inflation

posted by Katy Delay at 6:22 PM

0 comments

![]()

![]()

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}